Net-zero emissions, but how?

I bet, you wondered why net-zero is important or how to reach net-zero by 2050. To start with, the Paris Agreement, an international treaty on climate change, sets a long-term goal of limiting global warming to 1.5°C compared to pre-industrial levels to avoid the worst impacts of climate change. To achieve that goal, global emissions must be reduced by 45% by 2030 and reach "net-zero" by 2050. More than 70 countries and over 700 of the Forbes 2000 largest companies pledged to get to net-zero emissions. But, how can companies set the most cost-effective and realistic yet robust targets to reach net-zero? The answer lies in the science-based targets. In this blog, we’ll strive to explain in simple terms the steps from a measurement of your company’s GHG inventory to addressing your residual emissions.

Net-zero

According to IPCC special report on the impacts of global warming of 1.5 °C, the maximum temperature reached is determined by cumulative net global anthropogenic CO2 emissions up to the time of net zero CO2 emissions.

Net zero carbon dioxide (CO2) emissions are achieved when anthropogenic CO2 emissions are balanced globally by anthropogenic CO2 removals over a specified period.

Step 1: Measuring GHG Emissions

The very first step should be measuring your company’s GHG emissions because “what gets measured, gets managed.” Your company needs to select a baseline year, a most recent year that could provide necessary and verifiable data for purpose of measuring your Scope 1, 2 and 3 emissions (see the below excerpt from the GHG Protocol). The baseline year will also become your reference point in tracking your progress towards your emission goals. Collecting data for the Scope 3 emissions can be, indeed, challenging as sources are not controlled or owned by your organization.

Scope 1 (Direct GHG emissions)

Emissions from your activity and sources directly controlled and owned by your company

Scope 2 (Indirect GHG emissions)

Emissions indirectly generated by your company’s purchase of energy including gas, electricity and power

Scope 3 (Other indirect GHG emissions)

Emissions from sources not controlled or owned by your company, including purchase of products from your suppliers or from your customers using your products

There is a wide range of sources your company could use to calculate your GHG inventory that includes all major GHGs covered by the Kyoto Protocol. Among those standards and guidelines, GHG Protocol supplies the world's most widely used GHG accounting standards (such as the GHG Protocol Corporate Standard, Scope 2 Guidance, and Corporate Value Chain (Scope 3) Accounting and Reporting Standard). According to their data, in 2016, the GHG Protocol was used by around 92% of Fortune 500 companies.

The GHGs covered by the Kyoto Protocol

The major GHGs are carbon dioxide (CO2), methane (CH4) and nitrous oxide (N20). Less prevalent - but very powerful - greenhouse gases are hydrofluorocarbons (HFCs), perfluorocarbons (PFCs) and sulphur hexafluoride (SF6).

However, the measurement can be a time-consuming process and/or you may lack the necessary expertise to calculate your GHG inventory. In that case, your company has a choice of hiring independent assessment providers who can identify what data is needed, support your data collection process and calculate your emissions. The measurement is a requisite for companies that want to set realistic and robust GHG reduction targets based on science.

Step 2: Setting GHG Reduction Targets

As mentioned before, to accelerate global climate action to fight climate change, it’s critical that companies set science-based emission reduction targets. The emission targets are considered science-based if they are aligned with the goals of the Paris Agreement to limit global warming well below 1.5°C.

In terms of available sources, the Science Based Targets initiative (SBTi)’s Corporate Net-Zero Standard is the most widely used standard for formulating net-zero targets consistent with the Paris Agreement and backed by science. Approximately 2,200 companies representing over a third of the global economy’s market capitalization worked with SBTi in 2021. The above Standard stipulates that (1) near-term targets should be set for the next 5-10 years. Also, it must cover at least 95% of Scope 1 and 2 emissions of your entire organization. Then, companies have to set (2) long-term targets for their emission reduction consistent with the global net zero targets by 2050 or sooner. Similarly, the targets have to cover at least 95% of Scope 1 and 2 emissions and 90% of Scope 3 emissions.

It must be noted that carbon offsets are not counted as emission reductions in achieving science-based targets. In other words, companies have to include emission reductions from their operations or value chains. Companies can validate their science-based targets through the SBTi or another independent verifier. In short, the adoption of science-based targets can certainly put your organization ahead of your competition, increase investor confidence, save costs in achieving net-zero and enhance your resilience to future regulations concerning carbon emissions.

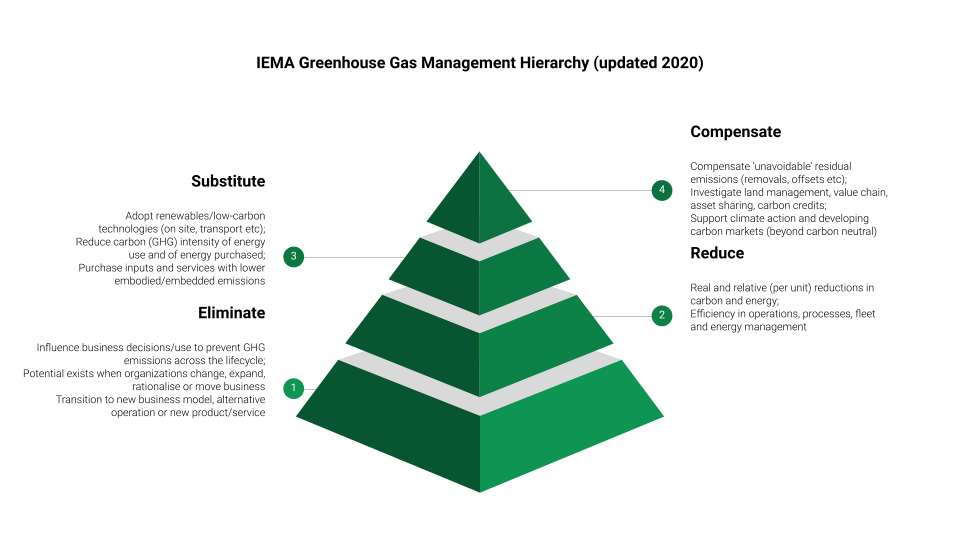

Step 3: Offsetting Residual GHG emissions

Under the mitigation hierarchy (see the cover picture), companies must first set science-based near and long-term targets to avoid (or eliminate), reduce and replace (or substitute) emissions in their value chains. With that said, most companies cannot completely eliminate their operational GHG emissions. The SBTi points out that companies can reduce their emissions by at least 90% by using near and long-term science-based targets, but some residual emissions will still remain. Moreover, long-term targets could be compromised due to unprecedented or unforeseen future economic, political, or societal events such as the COVID-19 pandemic or the Ukraine war. As a result, companies might need to address their residual emissions through carbon offsets.

Carbon offsets can also play an important role in raising emission reduction targets in developing countries. That means companies can use carbon credits to offset their residual emissions but also finance additional emission reductions outside the scope of their science-based targets. The voluntary carbon markets are estimated to grow by a factor of 15 times or more by 2030 and by a factor of up to 100 by 2050 (Source: McKinsey). This shows the importance of offsets in driving ambitious climate action in all parts of the world. Prior to turning to a carbon market and buying carbon credits, read our first blog on potential issues of current markets. We’ll dig deeper into how carbon markets work in our next blog. Stay tuned!

Final Remarks

To remain in line with the path to keeping the global temperature rise to 1.5°C, global emissions must reach "net-zero" by 2050 and be reduced by 45% by 2030. Hence, companies, cities and countries need to urgently adopt science-based targets which can enable us to reach our net-zero targets by 2050 or sooner in the most cost-effective, realistic and robust way. Furthermore, it can create opportunities to move one step further and contribute to reaching net-zero targets in developing nations by investing in mitigation action outside our value chains, possibly through carbon credits. Our team at URECA can help you each step of the way. Let’s get guided by science.

Comments ()